Learn how you can reduce your total loan cost with Dave Ramsey’s 7 steps for effective financial management and smart borrowing.

You know precisely where I was if you have ever gazed at a stack of loan statements and questioned whether you will ever see the end of it.

Stressed and overwhelmed by loan debt, I felt caught in a never-ending cycle of interest payments.

Things started to shift only when I came about Dave Ramsey’s 7 Baby Steps.

Using these guidelines, I will walk you through my path of financial transformation in this post, offering personal tales and ideas that might help you to address the question: How can you reduce your total loan cost?

Let’s get started.

Article Breakdown

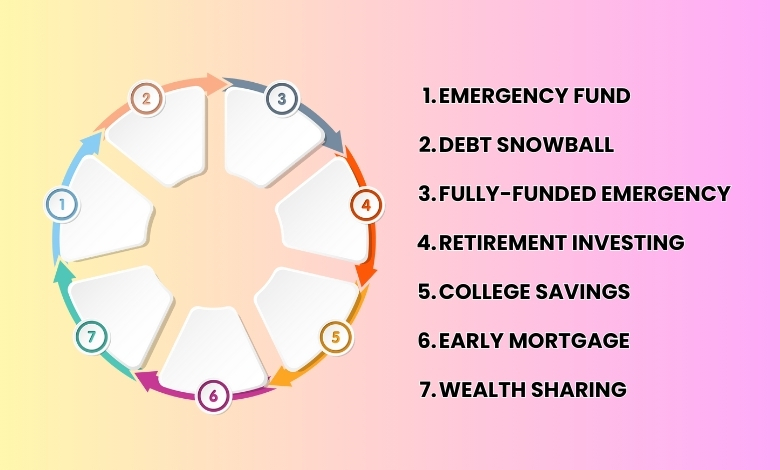

What Are Dave Ramsey’s 7 Baby Steps?

Let’s first consider what these actions mean to grasp their influence. The 7 Baby Steps were created by financial guru Dave Ramsey, known for his pragmatic approach to personal finance, to enable others to reach financial freedom.

These actions map from financial uncertainty to stability and wealth-building.

Every action is meant to build on the last, therefore laying a strong basis for next financial success. These are not just ideas; rather, they are practical plans of action meant to significantly lower loan expenses.

Using the 7 Steps: How Could I Cut My Overall Loan Cost?

Let us now explore how each of these actions significantly helped me to lower my loan debt and improve my general financial situation.

Baby Step 1: Emergency Fund to Prevent Further Debt

My first aim, beginning with Baby Step 1, was to save $1,000. Though little, this emergency money was a necessary safety net that gave me peace of mind.

Having this buffer meant I wouldn’t have to go into further debt when unanticipated costs like medical bills or auto repairs emerged. I could boldly pay for these expenses instead of grabbing a credit card or loan, therefore halting my financial advancement.

This first move was absolutely vital in avoiding fresh debt and provided me the confidence I needed to face other major financial obstacles.

Baby Step 2: Debt Snowball Method

My path started in Baby Step 2: using the debt snowball approach to pay off all of my debt. Regardless of interest rates, this approach meant ranking my debts from smallest to largest and targeting the smallest ones first. Eliminating a debt, no matter how little, was a psychological triumph that really drove me to move ahead.

I focused those payments toward bigger loans as I paid off the smaller ones, therefore greatly lowering the total interest I was paying. This strategy not only accelerated loan pay-off but also gave me a sense of accomplishment that drove me across more difficult financial obstacles.

Baby Step 3: A Fully Realized Emergency Fund

Baby Step 3 concentrated on saving three to six months’ worth of living expenses while debt was reducing. My financial burden was much lessened by this totally funded emergency fund.

Knowing I had a cushion for life’s fluctuations—such as job loss or unanticipated expenses—meant I could finally turn my attention to other financial objectives, including reducing my student loan rate.

Knowing I wouldn’t be knocked off track by unanticipated events, this safety net let me take measured risks in both my personal life and career.

Baby Step 4: Investing for Retirement Under Debt Management

It changed everything to commit 15% of my income toward retirement. Investing while remaining under debt first seemed contradictory, but I soon discovered that this was a necessary component of my whole plan.

This phase helped me to realize the need of future planning rather than concentrating only on present financial responsibilities. Prioritizing my retirement savings helped me to be financially secure over the long run and helped me to see the potential of compound interest.

This investment mentality changed my perspective on money and enabled me to reconcile long-term benefits with temporary sacrifices.

Baby Step 5: Juggling Debt and Children’s Education

For those with children, Step 5 is saving for their college fund—a top priority for my household. Though my main concentration was on lowering debt, I soon saw how important it is to start thinking ahead for my children’s future schooling.

Gradually helping this fund helped me to prevent the possibility of future loans for study and guaranteed that my children would have access to opportunities free from student debt.

This proactive attitude not only helped me to relax financially but also let me be a good example for my children about financial responsibility and literacy.

Baby Step 6: Early Mortgage Payoff

Another big turning point in my financial path was early mortgage payoff. I greatly lowered the total interest paid over the loan by deliberately making extra payments toward the principal.

This strategy not only cut my overall loan load but also freed extra money for side businesses or real estate investing, thereby growing wealth.

Owning my house outright brought an unbounded sense of relief that inspired me to seek even more financial freedom.

Baby Step 7: Creating Wealth and Giving Back

Approaching the last stage was a fresh start as much as a release. Building wealth and giving back helped me to find financial freedom and a sense of direction beyond just numbers.

This phase evolved from simply building wealth to significantly changing my life and the lives of others.

Whether by means of philanthropy, mentoring, or sponsoring local projects, the capacity to give back enhanced my journey and reinforced the concept that true financial success is about making a difference.

Important Lessons

Applying Dave Ramsey’s methods taught me these things:

Additional Information

Consult the following materials to help you grasp Dave Ramsey’s Baby Steps and other debt-reduction techniques: